What Drives Innovation in Cardiovascular Health?

Nicole Chen, M.B.A.

Duke University Fuqua School of Business

Cardiovascular Innovation Funding

Cardiovascular innovation is sourced through numerous avenues, including research and development arms of large corporations, government agencies, universities and research foundations. For most of these innovation sources, the parent company or organization itself has a budget set aside to fund the internal generation of new ideas. An alternative source of innovation, where this internal funding support does not exist, is independent startups. Despite this lack of funding support, startups have several advantages of being independent. Their founder-owned governance structure, for example, allows them the freedom and agency to be more flexible, risk-taking and innovative than large corporations. However, the lack of internal funds can be a significant hurdle, and as a result, startups often rely on external sources of capital, such as venture capital (VC) firms, to support them.

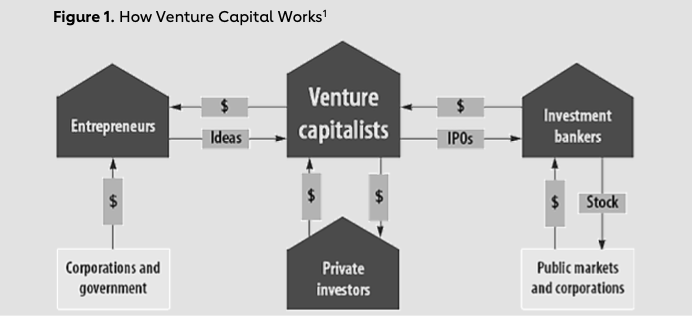

The VC industry has four key players: entrepreneurs, investment bankers, private investors and the venture capitalists. In this market, venture capitalists act as intermediaries between these players, providing entrepreneurs with funds, mentor networks and expertise, providing private investors or limited partners with high returns, and providing investment bankers with startups to sell or take to the public market (Figure 1).

By providing the financing necessary for startups to succeed, VC firms play an outsized role in funding innovations. This chapter explores the role of VC in both encouraging and hindering innovations in cardiovascular medicine.

Venture Capital Trends in Health Care and Cardiovascular Medicine

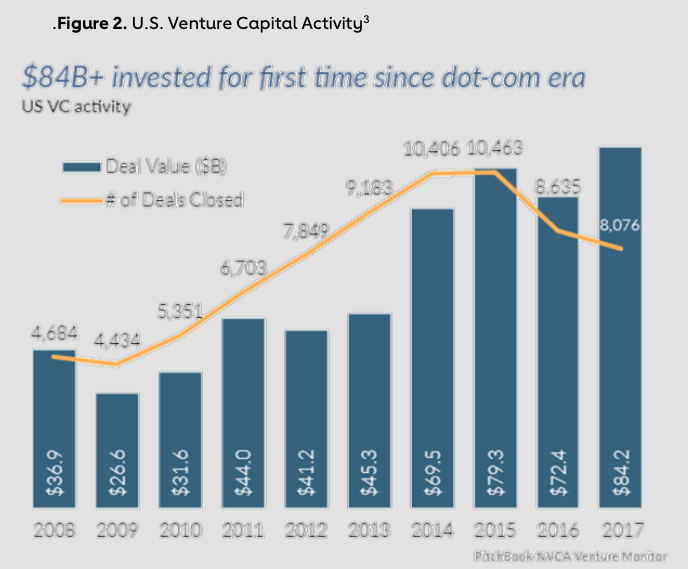

Since the early 2000s, VC investments in the U.S. have surged, nearly doubling in less than a decade from 4,684 deals worth $36.9 billion in 2008 to 8,076 deals worth $84.2 billion in 2017 (Figure 2).2

The health care industry has seen continual growth in VC investments, specifically in the life sciences and biotechnology space. In 2017, $17.9 billion in VC was invested in life science companies, a 48% increase over 2016 investment levels. By comparison, overall venture funding across industries grew only 16% from 2016 to 2017.4 Before this upward trend in health care funding, VC funding for products that required longer-to-market timelines and intense upfront capital had historically been overlooked. This chapter explores how initiatives such as venture philanthropy, M&A activity and alternative drug-development models have allowed for and supported this growth in health care VC investments.

Challenges in Health Care Funding

Health care ventures primarily fall into three categories: biotechnologies, medical devices and digital health solutions. As discussed below, due to the biological and medicinal nature of health care technologies, these ventures face distinct challenges, long regulatory pathways and funding hurdles unique to the health care industry.

Pharmaceutical drugs, for example, require many levels of research and clinical validation, including in vitro cell culture research, in vivo animal model research, several phases of clinical trials and so on before launch. This drug development process takes on average more than a decade from initial discovery to market and can cost companies millions of dollars before a product can even begin to be marketed and distributed. In fact, the average cost of research and development of a successful drug is estimated to be approximately $2.6 billion.5 Note this average cost includes funds invested into millions of failed compounds that are tested each year during the initial discovery and research phases but that ultimately do not receive approval to launch in the market. This research and evaluation process lends itself to a 13.8% clinical success rate and consequently drives hesitancy in the funding market to invest in clinical research.6 The low clinical success rate coupled with long and costly clinical runways lead venture capitalists to view biotechnology startups as highly risky ventures.

For medical devices, the hurdles in the research and development process are similar but less risky. Medical devices take, on average, three to seven years to go to market — about half the time pharmaceutical drugs take to launch.7 Moreover, medical device companies commonly develop new products that are iterations of existing devices. The FDA views these iterations as add-ons to existing products in the market that have already demonstrated regulatory safety and efficacy, and thus require fewer clinical trials and less evidence for regulatory approval. This shorter pathway to market has historically made medical device startups more attractive to venture capitalists than pharmaceutical startups.8

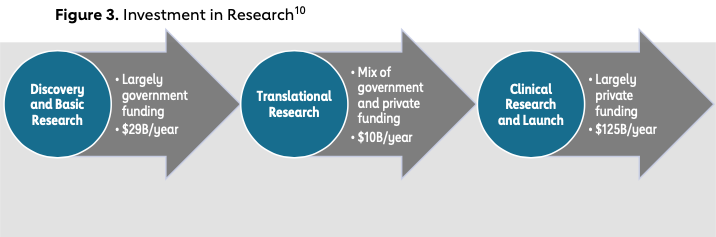

Analyses of funding support by research phase have found that funding at the translational research phase — a critical phase required to move a product to the final stage of research and consequently launch — is particularly sparse for both pharmaceuticals and medical devices. This disparity has come to be known in the health care industry as the “translational research gap.“ Specifically, whereas approximately $29 billion is invested per year in products in the discovery and basic research phase and over $125 billion is invested in products in the clinical research and launch phases, only $10 billion per year is invested in products in the translational research phase. 9 In the discovery and basic research phase, federal agencies, the National Institutes of Health and the Department of Defense in particular, provide health care ventures significant support. On the other end, VC firms begin investing in health care ventures once the venture is derisked and is in the final stages of development, closer to launch. This investment timing results in a lack of funding in the middle, the translational research gap, also referred to as the “funding gap“ or the “Valley of Death“ (see Figure 3). At a time of development when proving clinical success is critical to garnering further financial and clinical support, this gap presents a significant hurdle and has historically been a barrier for health care ventures to succeed.

Funding by Disease Indication

These funding challenges pose an even greater threat in certain health care sectors due to the availability and focus of capital by disease indication. From a federal incentive standpoint, oncology and orphan or rare disease indications take a significant share of health care investments relative to cardiovascular indications.11 In fact, the NIH reports that whereas 8% of funds per year are allocated for oncology and rare diseases, only 1-2% of funds per year are allocated for cardiovascular diseases —percentages that have remained relatively stable since 2013.12

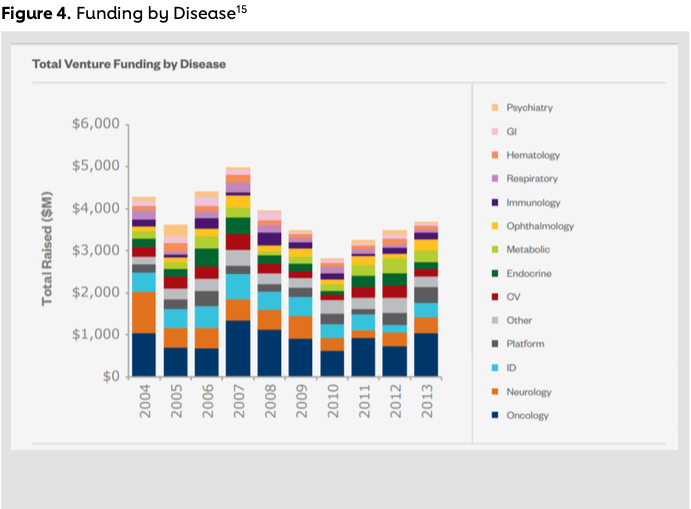

In 2015, the Biotechnology Industry Organization (BIO) conducted a study to understand private investor trends in the health care industry and to evaluate the breakdown of investments in specific therapeutic indications. The study analyzed data from four VC databases and included 38 billion VC dollars invested in more than 1,200 U.S. drug companies for a 10-year period from 2004 to 2013. The BIO study findings showed a large proportion of health care VC dollars, upwards of 20%pc, invested in oncology and rare disease ventures. By comparison, only 6% of health care VC dollars in 2004-2013 were invested in cardiovascular ventures.13

To highlight this difference further, one can look at investment patterns from VC firms themselves. The most active investor in pharmaceutical companies since 2013 has been New York-based investor OrbiMed Advisors. OrbiMed’s portfolio shows investments in companies pioneering a variety of cancer therapies such as targeting the DNA damage response pathway (Sierra Oncology, IPO 2015), gene regulation (PMV Pharmaceuticals) and T-cell therapy (Adaptimmune, IPO 2015). Furthermore, OrbiMed has made deals with companies working in rare diseases (Audentes Therapeutics, Dimension Therapeutics), infectious diseases (Nabriva, IPO 2015) and ophthalmology (Kala Pharmaceuticals). By comparison, OrbiMed, along with the top active life science investors, including Novartis Venture Fund, New Enterprise Associates and RA Capital Management, to name the top four, have not focused on cardiovascular research14 (see Figure 4).

This disparity in the distribution of investment dollars by disease state stands in contrast to the prevalence of cardiovascular disease and cancer. Heart disease is the leading cause of death for both men and women in the U.S., with approximately 640,000 people dying of heart disease in the U.S. every year.16 Cancer mortality rates closely follow, with approximately 596,000 cancer deaths in the U.S. per year.17 The dichotomy between low venture investment dollars despite a similar disease prevalence ultimately suggests cardiovascular research continues to be relatively underfunded. In the European Heart Journal, Dr. David Garcia-Dorad attributes this disproportionately low funding of cardiovascular research to five factors: one, the human emotional factor associated with cancer; two, the attractive economic and business implications of cancer treatments for drug companies driven by this emotional factor; three, the false perception that cardiac diseases are preventable and declining; four, the acute nature of some cardiac conditions, such as acute myocardial infarction; and five, the late adoption of molecular and genetic innovations to cardiovascular research.18 The last suggests an urgency to increase cardiovascular funding levels to allow for innovation in cardiovascular research to catch up with treatment innovations in other disease indications.

Venture Capital Funding of Cardiovascular Medicine

A few notable VC investments have been made in cardiovascular medicine in recent years. Kleiner Perkins, Caufield, and Byers, one of the largest and most established VC firms based in Silicon Valley, specializes in incubation, early-stage and growth companies and has a subsector of investments dedicated to life sciences and digital health investments. In 2012, Kleiner Perkins was part of a private equity funding round for CardioDx, a cardiovascular genomic diagnostics company that provides clinicians with information to enhance patient care through clinical genomic testing. Since 2012, CardioDx has raised over $305 million through multiple funding rounds, closing a series D funding round in 2016. In 2015, CardioDx signed a multi-year agreement with Quest Diagnostics that will expand patient and clinician access to CardioDx’s blood test for coronary artery disease.

Note that from a venture capitalist perspective, CardioDx is a cardiac diagnostic tool, which requires a shorter regulatory and clinical runway than pharmaceutical drugs, biotechnologies or medical devices. Furthermore, Kleiner Perkins indicated a trend toward digital health products in its 2017 Internet Trends Report, citing that future health care delivery innovations will be driven by digital inputs and data accumulation.19 This trend suggests cardiovascular innovations, particularly therapeutics that do not have digital health or data-driven business models, may continue to be underfunded.

Alternative Funding Models in Cardiovascular Medicine

For cardiovascular innovations for which initial funding across all stages of research is low, finding the appropriate timing of funding is critical. Strategies and market responses to fill this capital shortage include foundations, incubators, angel groups and other organizations that have developed supplementary funding models designed specifically to address this research gap. With a focus on startups in the translational research phase, these funding models disrupt traditional VC firms by building industry-expertise networks that provide cardiovascular startups the right guidance to succeed. Through these networks and by being mission-driven rather than financial returns-focused, these funding models have emerged as a disruptive and more targeted approach that is “better aligned with and has the capability to support technology and startup development in the early stages.“20 By supporting early-stage startups through the translational research phase, these funding models ultimately enable startups to develop to a stage attractive to VC firms or large corporations for potential acquisition. Of note, the recent uptick in cardiovascular M&A activity indicates early success in these efforts. For example, corporations such as Medtronic, Boston Scientific and Teleflex that have already made capital and research investments in the cardiovascular space have increased their focus on small medical-device startups that require additional resources to fill the translational gap.21 Investing in early-stage companies also allows larger biopharma and medical-device companies to replenish their pipelines. For example, Symetis, which was recently bought by Boston Scientific for its percutaneous heart valve replacement solutions, was backed by BioMed Ventures, Novartis Venture Funds, Banexi Ventures and NBGI Ventures.

One example of venture philanthropy that is focused on bringing cardiovascular innovations through the translational research gap is Broadview Ventures.

Case Study: Broadview Ventures

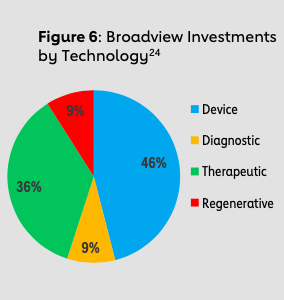

Boston-based Broadview Ventures was founded in 2008 by the Leducq Foundation with the mission of accelerating the development of technology for the diagnosis and treatment of cardiovascular, metabolic and neurovascular disease. Like a traditional VC firm, Broadview invests in startups through equity-based investments. However, unlike traditional VC firms, Broadview invests only in cardiovascular and neurovascular innovations.

Broadview’s origins from the Leducq Foundation drive this industry focus. Operating as a private foundation based in Paris, France, the Leducq Foundation was founded by French entrepreneur and industrialist Jean Leducq in 1996. Together with his wife, Sylviane, Leducq used proceeds from his family’s linen and uniform service business to build a foundation focused on funding international cardiovascular, metabolic and neurovascular research. Their mission, motivated by a multigenerational family history of cardiovascular illness, is to improve human health through international efforts to combat cardiovascular disease. As of 2015, the foundation had made 47 network awards totaling over $350 million, supporting hundreds of researchers at 123 institutions in 18 countries, and had established itself as a thought-leader organization in cardiovascular medicine.22

In 2008, the Leducq Foundation saw a need to fill the translational gap that was negatively impacting cardiovascular innovation, and created Broadview Ventures. Broadview considers itself a philanthropic venture firm whose investment funds originate from the Leducq Family Trust and whose investments are mission-based but made through equity and convertible notes. Broadview funds its portfolio through evergreen arrangements, supplying capital in incremental payments throughout the development phase of the product and reinvesting the funds when investments mature. Although structured independently, Broadview is able to be industry- focused and invest in early-stage products that bear exponentially more risk due to its resources and networks from the Leducq Foundation. The Leducq Family Trust serves as the sole shareholder of Broadview, establishing a synergistic relationship between Broadview and the Leducq Foundation, a unique departure from traditional for-profit VC firms. With the foundation’s support, Broadview can bear the long-term capital commitments required of early- stage investments in otherwise untapped areas of the market. Perhaps most importantly, Broadview also has access to world-class cardiovascular medicine thought leaders from the Leducq Foundation and its Strategic Advisory Board. Its expertise and relationships have powered Broadview’s success through every stage of investment from deal sourcing and diligence to investment counsel and portfolio company guidance. In return, the foundation gains financial investments in technologies that advance cardiovascular medicine.

By being philanthropic-driven, Broadview’s definition of success is social rather than financial with the primary goal of having a “social impact and improving patient care.“ Chris Colecchi, managing director at Broadview Ventures, further emphasized this point when he shared that Broadview is evaluated for the number of patients it touches rather than its financial returns. Furthermore, despite investing in cardiac and neurovascular indications across various technologies, Broadview does not attempt to balance these innovations, as some traditional VC firms may do to diversify their portfolios. Instead, Broadview focuses on innovations that have the potential to impact patient therapy or the standard of care and that require early-stage funding to become attractive to other VC firms or larger corporations for acquisition in later stages.

Dr. Joe Loscalzo at Brigham and Women’s Hospital previously served as a member of the Strategic Advisory Board at the Leducq Foundation and is now a member of Broadview’s Strategic Advisory Board. He posits that four factors ultimately give Broadview a competitive advantage over conventional VC firms: One, Broadview’s not-for-profit, evergreen fund structure aligns the firm’s incentives more closely with the incentives of startups; two, an exclusive cardiovascular and stroke focus develops necessary industry networks and expertise; three, international scientific advisers and the Leducq Foundation bring a wealth of knowledge and access to technological innovations; and four, Chris Colecchi and his team’s connections establish critical relationships for co-investments.

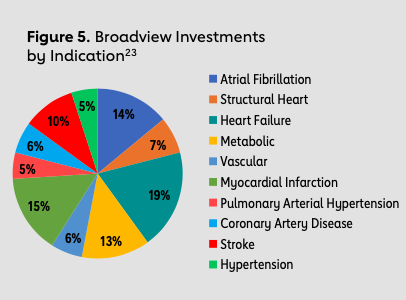

Notable exits of Broadview-backed companies include four with cardiovascular indications (Apama Medical, Capricor, CardiAQ Valve Technologies and Provasculon) and two with neurovascular indications (Pulmokine and Remedy Pharmaceuticals). In 2017, Boston Scientific acquired Apama Medical — designer of 360-degree ablation technology used to treat atrial fibrillation — for $300 million, and Biogen acquired Remedy Pharmaceuticals’ lead product Cirara for $120 million. The target indication for Cirara is large hemispheric infarction, a severe form of ischemic stroke, and Cirara was recently granted both Orphan Drug Designation and Fast Track Designation by the FDA. Broadview’s early financial support and mentorship in these companies ultimately allowed these technologies to complete necessary milestones to be better poised for angel investors, VC investors and, later, acquisition. This advantage is especially critical for academic inventors who require support at the critical juncture of translational research to prove clinical success to investors and get one step closer to market. Furthermore, due to Chris Colecchi and Broadview’s well-known expertise in cardiovascular medicine, an investment from Broadview also signals and mitigates the risk to conventional VC investors who are thinking of co-investing in a venture. From the standpoint of other VC firms, Broadview’s expertise serves as an indicator of a cardiovascular innovation worth investing in. In fact, as of March 2018, Broadview had invested $48.5 million in initial investments, leading to a 10x multiple in over $488 million leveraged into later grants, co-investments and follow-ons.

The story of CardiAQ Valve Technologies, one of Broadview Venture’s first success stories, emphasizes the importance of early-stage investing in cardiovascular medicine and how it can continue to reverberate through different stages of development. In 2008, Broadview was introduced by CardiAQ Valve Technologies — at that time, a surgeon and business executive working part-time to develop a percutaneous mitral valve implantation device. After several rounds of due diligence and advisor reviews, Broadview made a $750,000 seed investment in CardiAQ to develop a device prototype and conduct early animal testing. Both steps were critical to not only moving the product along, but also attracting additional investments that would fund later progress. Sure enough, in 2011, CardiAQ successfully raised a $5 million Series A financing round from angel investors and Broadview. This infusion of funds allowed the company to build research facilities, develop the first-ever transcatheter mitral valve replacement (TMVR) in a porcine model and perform a human valve implantation. The progress demonstrated after the Series A funding round attracted several more VC investors for a Series B financing round, during which $37.3 million was raised. In 2015, Edwards Lifesciences acquired CardiAQ for $400 million. Today, CardiAQ’s valves are being tested in clinical trials and show promise in providing a TMVR technology to solve mitral regurgitation.25 The history of CardiAQ highlights how funds, invested at an early stage and made possible through philanthropy, can enable entrepreneurs to overcome the translational research gap and move forward through clinical research to launch. On a macro level, this process ultimately enables the funding of higher-risk but higher-reward research that has the potential to drive innovations in cardiovascular medicine.

New Models

Over the last few years, alternative models to traditional VC similar to Broadview Ventures have emerged that promote health care innovations and address funding gaps in various research phases. However, not all of them target the translational research funding gap like Broadview, as shown by Roivant Sciences’ unique approach to drug development.

In contrast to Broadview Ventures, which targets early-stage companies, Roivant Sciences identifies late-stage drug candidates in the pipelines of external organizations that would otherwise be abandoned due to corporate and financial limitations, and brings them to market. Often, promising drug candidates are discovered but abandoned by the parent company or academic institution due to lack of targeted disease-area focus, funding and development resources. Founded in 2014 by CEO Vivek Ramaswamy, Roivant identifies these promising drug candidates, partners with their parent organization to acquire them and then rapidly works to bring the candidates to market. Deals struck with parent organizations are unique partnerships that resemble a hybrid between acquisition and VC deals. Roivant’s recent acquisition of Poxel’s phase-3-ready Type 2 diabetes drug imeglimin, for example, was for $600 million in milestones, $15 million for a 6% stake in Poxel in return for the rights to imeglimin in certain Asian countries, and $35 million up front. In return, Poxel will contribute $25 million to clinical trials, but Roivant will bear the financial and development process lifting beyond the capabilities of Poxel. Roivant will then plan to move imeglimin into a U.S. and European phase 3 program next year.26

Drug candidates such as imeglimin are accelerated through decentralized subsidiary companies that Roivant has dubbed “Vants.“ Vants are wholly or majority-owned subsidiary companies held under the general corporate umbrella of Roivant. To date, Roivant has seven Vants — Axovant, Dermavant, Enzyvant, Metavant, Myovant, Urovant and Datavant — with one drug candidate with a cardiovascular indication in phase 1 trials for pulmonary arterial hypertension.27 Each Vant is responsible for bringing its drug candidate to launch, allowing each Vant to take ownership of drug development while being backed by Roivant resources and expertise. This business model creates a unique entrepreneurial culture resembling individual startups, and allows for the development of focused, passionate teams and, ultimately, expedited drug development. Perry Clarkson, a business development associate at Roivant, emphasized that in many ways, each Vant thinks and acts like a small startup but with the resources of a well-established, large company. On a broader level, this Vant structure also enables Roivant, as the parent company, to take bets where others may not be willing to risk investment. Similar to Broadview Ventures, whose business model capitalizes on industry expertise for successful investments in cardiovascular innovations, Roivant Sciences’ business model enables independent Vants to bring innovations to market faster and with fewer resources.

Conclusion

As health care innovation continues to blossom at a rapid pace, health care venture funding has followed suit, reaching a growth rate three times the rate of venture funding in all industries. Despite this growth, investments in targeted disease areas have proved to be unequal because of investor interest, disease-specific challenges and outside resource constraints. We’ve thus seen specific health care investments and interest centered on oncology and rare diseases, as well as digital health and remote monitoring in cardiovascular medicine. In reaction to this environment, alternative funding models have emerged, specifically in cardiovascular therapeutics, to combat uneven investor funding and spur continual cardiovascular innovations. These models include targeted early-stage investments to overcome the translational research gap, as with Broadview Ventures; increased M&A activity from medical device companies; and unique business models to expedite drug development, such as Roivant Ventures. Going forward, it will be interesting to note how investments in cardiovascular innovations change as the miniaturization of heart devices, regenerative cardiovascular medicine and remote monitoring technologies continue to develop and impact the practice of cardiology.

Endnotes

- B. Zider, “How Venture Capital Works,“ 1998. https://hbr.org/1998/11/how-venture-capital-works.

- Pitchbook. Pitchbook – NCVA Venture Monitor 4Q 2017. Pitchbook, National Venture Capital Association, 2017.

- Ibid.

- Ibid.

- PhRMA, “Biopharmaceutical Research Development: The Process Behind New Medicines,“ PhRMA, 2015.

- Cross, Ryan. “Drug Development Success Rates Are Higher than Previously Reported.“ CEN RSS, American Chemical Society, 7 Feb. 2018. cen.acs.org/articles/96/i7/Drug-development-success-rates-higher.html.

- G.A. Van Norman, “Drugs, Devices, and the FDA: Part 2: An Overview of Approval Processes: FDA Approval of Medical Devices.“ JACC: Basic to Translational Science (2016): 277-287.

- G. Snyder, P. Arboleda and S. Shah. “Out of the Valley of Death: How Can Entrepreneurs, Corporations, and Investors Reinvigorate Early-Stage Medtech Innovation?“ Deloitte, 2017. https://www2.deloitte.com/content/dam/Deloitte/us/Documents/life-sciences-health-care/us-lshc-medtech- innovation.pdf

- Milken Institute, “Fixes in Financing: Financial Innovations for Translational Research,“ Milken Institute FasterCures, 2012. http://www.fastercures.org/assets/Uploads/FixesInFinancingWeb.pdf

- Ibid.

- J. Norris et al., “Trends in Health Care Investments and Exits 2018,“ Annual Report, Silicon Valley Bank, 2018.

- National Institutes of Health, “Estimates of Funding for Various Research, Condition, and Disease Categories (RCDC),“ July 3, 2017. https://report.nih.gov/categorical_spending.aspx

- D. Thomas and C. Wessel, “Venture Funding of Therapeutic Innovation,“ Washington, D.C.: Biotechnoloy Industry Organization, 2015.

- CB Insights, “Seeking a Cure: The Most Active Pharma Investors In One Infographic,“ June 8, 2017. https://www.cbinsights.com/research/pharma-drug-startups-most-active-investors/

- Thomas and Wessel, “Venture Funding.“

- Centers for Disease Control and Prevention, “Heart Disease Facts,“ Nov. 28, 2017. https://www.cdc.gov/heartdisease/facts.htm

- National Cancer Institute, “Cancer Statistics,“ March 22, 2017. https://www.cancer.gov/about- cancer/understanding/statistics

- D. Garcia-Dorado. “Insufficient Cardiovascular Research and Development Funding.“ OUP Academic, Oxford University Press, 21 Jan. 2017. (academic.oup.com/eurheartj/article/38/1/10/2936214)

- M. Meeker, Internet Trends 2017 – Code Conference. San Francisco: Kleiner Perkins, 2017.

- Innovosource, “University Gap Funding: Mind the Gap,“ 2016. http://www.gapfunding.org/mindthegap/.

- CB Insights, “The Race To Acquire Medical Device Startups In One Graphic,“ May 3, 2017. https://www.cbinsights.com/research/medical-device-acquisition-timeline/

- Leducq Foundation, “History,“ 2018. https://www.fondationleducq.org/about/history/

- Broadview Ventures. Annual Report 2017. Boston: Broadview Ventures, 2017.

- Ibid.

- T. Casey, “Proceed With Caution: Will Transcatheter Mitral Valve Interventions Be Cardiology’s Next Big Win?“ Cardiovascular Business, Feb. 28, 2018. http://www.cardiovascularbusiness.com/topics/structural-congenital- heart-disease/proceeding-caution-will-transcatheter-mitral-valve

- N.P. Taylor, “Roivant Expands into Metabolic Diseases with $650M Poxel Diabetes Pact,“ Fierce Biotech, February 12, 2018. https://www.fiercebiotech.com/biotech/roivant-expands-into-metabolic-diseases-650m- poxel-diabetes-pact

- Roivant Sciences, Roivant Sciences, 2017. http://roivant.com/

-

-

Driving Innovation

-

Innovations in Cardiovascular Health

-

The Role of Physicians in Driving Innovation

-

The Role of Patient Groups in Driving Innovation

-

Clinical Innovations in Cardiovascular Health

-

What Drives Innovation in CV Health?

-

The Rise of Academic and Contract Research Orgs

-

Federal Regulations as Accelerators

-

Reimbursement Models

-

Consumer Technology

-

Training Cross-Disciplinary Innovators

-

Conclusion